I didn't get any money from the sale. $500K was paid by Qenta into the bank's account. So that was extra capital to payoff customers. Another $750K was supposed to be paid, but Qenta is not paying due to the extra costs they incurred over the past two years. I also sold the bank's office furniture for $50K. That went into the bank's account as well.ehhmm sorry PS why didnt you send paper checks to your customers lol???? Then they would have been able to cash them at their bank.

No you wanted to SELL the client book to gain money out of it on the shoulders of your LOYAL customers for years.

Our valued sponsor

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Euro Pacific bank is a scam

- Thread starter OffshoreCorpTalk

- Start date

-

- Tags

- euro pacific bank

He sent me an email. So I posted a summary of what he wrote.Alpinist: Schiff is very active in this forum and will just avoid responding to your requests for documentation regarding the sudden "Brent de Jong, CEO of Qenta email telling me everything is fine".

The money went to the bank, to further protect customers. Not one penny went to me. Also, customer funds were going to transfer directly into segregated accounts at a Qenta subsidiary for each Opt in customer. But that changed as a result of the Portugese government freeze of the Novo account. There was no way to have anticipated this.That is incorrect (and Peter knows it too!): The purchase and assumption agreement dated September 30, 2022, between EPB (seller) and Qenta (buyer) states that Qenta took over opt-in customers (and schiff was paid USD 1.25mll), with no guarantee of protection for them. Section 7.1(b) clearly states that "purchasers shall indemnify and hold harmless seller and sole shareholder from and against any and all losses which such person may suffer… relating in any such case to the assets or the liabilities assumed by purchasers at closing."

Also, Peter is not telling the truth. This document (which has been published here) does not mention segregation of accounts even once!

No one on this board should be upset at me or anyone that worked at Euro Pacific Bank. Corrupt government officials and journalists are 100% responsible for this situation. So direct your anger at them. They deserve it.

There are two key documents:

- "Liquidation and Dissolution Plan for Euro Pacific Bank"dated September 9, 2022, signed by Peter Schiff, Lugo Mender (the receiver), and the OCIF commissioner.

- Section 2: "Sale of Assets" explicitly states that for opt-in customers, "G-Commerce DMCC, a wholly owned subsidiary of Qenta, Inc., has agreed to assume/buy all the bank’s deposit obligations of both cash and precious metals. G-Commerce DMCC is incorporated under the laws of Dubai, UAE."

- "purchase and assumption agreement"dated September 30, 2022, in which Euro Pacific Bank sells opt-in customers (among other assets) to Qenta.

- This agreement was signed by Peter Schiff and Brent De Jong.

- Section 7.1(b) indemnifies Schiff and Euro Pacific Bank from any losses that may occur after the transaction date (September 30, 2022).

Last edited:

The losses related to losses that Qenta may incur as a result of acquiring the assets. It has nothing to do with bank customer's losses. Again, Qenta was setting up accounts for each Opt in customer. Qenta was going to convert all deposits into gold, via G-coin. That would have worked out well. Gold was $1,800 an ounce then. Now its $2,900. Customers would have left the gold in their G-coin wallets, or liquidated it and withdraw the balance in cash to any alternative financial institution. That was the plan. The Portugese Government got in the way due to the fraud committed by the OCIF Commissioner, the IRS, the other J5 Chief, and the media.

However, it looks like if anyone sues me or the bank for losses that related to the opt in customers, than Qenta has indemnified us for those losses. But the only way Opt in customers will lose money is if Qenta goes bankrupt before you get it back. In which case their indemnification will be worthless. However, according to the Qenta CEO, the company is not in financial trouble and is prepared to return all funds to customers.

However, it looks like if anyone sues me or the bank for losses that related to the opt in customers, than Qenta has indemnified us for those losses. But the only way Opt in customers will lose money is if Qenta goes bankrupt before you get it back. In which case their indemnification will be worthless. However, according to the Qenta CEO, the company is not in financial trouble and is prepared to return all funds to customers.

Last edited:

again at which bank are the Qenta assets being booked right now?

Did you ask for recent Qenta audited FS?

Did you ask for recent Qenta audited FS?

@PS thanks for giving the information. If Qenta is in no trouble why do they not answer (our) email? Why do they not send out a general message?The losses related to losses that Qenta may incur as a result of acquiring the assets. It has nothing to do with bank customer's losses. Again, Qenta was setting up accounts for each Opt in customer. Qenta was going to convert all deposits into gold, via G-coin. That would have worked out well. Gold was $1,800 an ounce then. Now its $2,900. Customers would have left the gold in their G-coin wallets, or liquidated it and withdraw the balance in cash to any alternative financial institution. That was the plan. The Portugese Government got in the way due to the fraud committed by the OCIF Commissioner, the IRS, the other J5 Chief, and the media.

However, it looks like if anyone sues me or the bank for losses that related to the opt in customers, than Qenta has indemnified us for those losses. But the only way Opt in customers will lose money is if Qenta goes bankrupt before you get it back. In which case their indemnification will be worthless. However, according to the Qenta CEO, the company is not in financial trouble and is prepared to return all funds to customers.

To say the truth, both EPB (Andrew) e Qenta (Raffy) replied to me very quickly. I asked about the homebanking then the discussion moved on my transfer lost in 2022....the problem is the lack of transparency to me, not how fast they reply (they did it, to me atleast)@PS thanks for giving the information. If Qenta is in no trouble why do they not answer (our) email? Why do they not send out a general message?

CEO of Qenta can say anything, whatever we wish to hear. The truth might be totally different and PS should understand this as well.

I was recently in Dubai and found out, that office is not there anymore. This is one clear evidence.

I was recently in Dubai and found out, that office is not there anymore. This is one clear evidence.

Last edited:

Here we have this article about Emergent Technologies and Qenta. Mentioning Brent de Jong as CEO of EmTech and Kerim Chouabi, CEO of Qenta CEE.A corporation registered in Delaware.

Yes, parts of Wirecard were sold to recover more funds. Wirecard had an Austrian GmbH that was used for administering the tech development of payment gateways and integrations. This was sold to Qenta same as Wirecard NA was sold to Syncapay, Wirecard AU was sold to Change Financial etc.

Since Delaware does not reveal the shareholders of a local corporation, how exactly have you figured out who owns Qenta Inc?

Within your screenshot of Qenta GmbH, it just shows that Kerim Chouaibi is the director of that German entity. So how does this provide evidence of him being the shareholder of either company?

Because the liquidation process could have been done more effectively, and, from provided information on 9Fraud, there was not really enough reason to block Qenta's acquisition and continuation of EPB business especially since there was going to be an immense capital increase that would protect clients.

https://www.prnewswire.com/news-rel...logy-driven-payments-solutions-301482341.html

This article is from February 2022, so before the welcome letter we received. (The news about EmTech end in February 2022: https://www.prnewswire.com/news/emergent-technology-holdings-lp/) This welcome letter stated that Qenta is a company based on Houston TX. That is not correct! Instead Brent de Jongs company resides there: https://contactout.com/Brent-De-Jong-7692123. So the clients of EPB were sent a welcome letter of Qenta (even with their brand name on top), but the company they were actually referrring to was the company of BdJ. So one can say, that this information at least was wrong! Which raises the question whether the agreement of the former EPB-clients to opt-in was based on false premises? And it also raises the question, whether the oversight of the OCIF in this process has failed? Which raises the question whether there is lawyer who is competent and willing and authorized to go against this?

Another hint that OCIF failed in its oversight responsibility. Brent de Jong: https://contactout.com/Brent-De-Jong-7692123CEO of Qenta can say anything, whatever we wish to hear. The truth might be totally different and PS should understand this as well.

I was recently in Dubai and found out, that office is not there anymore. This is one clear evidence.

When EPB presents a welcome letter of Qenta to its opt-in customers, but actually refers to Emergent Technology, without mentioning it: what is it? A lapse, a swindle or a fraud? - We are talking milllions of USD here! There has to be correct information!I don’t think Peter is a swindler or a scammer as he is a public person but it seems that he hasn’t been careful enough and by doing so put the opt-in funds at an unacceptable risk. I expect he will do is best to correct this. Stacking mistake on mistake would be foolish as there will be hundreds of opt-in customers going after him anywhere he shows up..

Absolutely correct! And EPB even had the audacity to provide its clients with wrong informations about Qenta (see my post above), while OCIF obviously did not pay attention to this fact!Peter’s pocket benefited from Qenta’s bizarre 'opt-in' concept,let’s not forget that! This report (https://epbprliquidation.com/wp-content/uploads/07-17-2023-EPIB-Trustee-Case-Progress-Report.pdf) reveals that 1,702 customers effectively sold themselves to the devil (Qenta), and Peter was paid USD 1.25 million for it. If no one had opted in, Peter wouldn’t have received that payout. That’s why there was so much cheap sales talk to lure customers into Qenta, which ALSO benefitted Peter

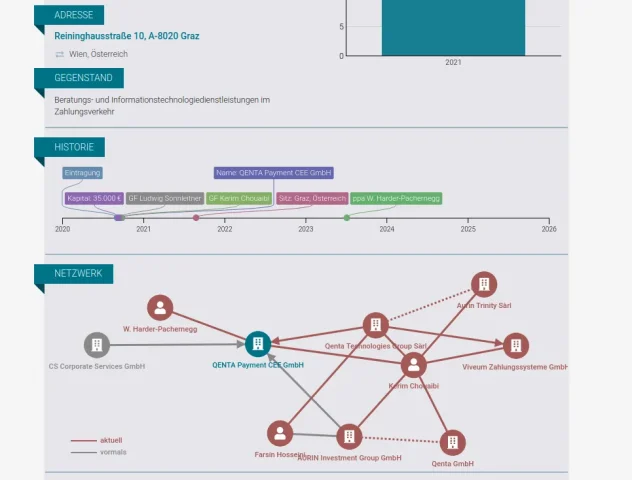

See below: https://www.northdata.de/QENTA Payment CEE GmbH, Graz/539960iA corporation registered in Delaware.

Yes, parts of Wirecard were sold to recover more funds. Wirecard had an Austrian GmbH that was used for administering the tech development of payment gateways and integrations. This was sold to Qenta same as Wirecard NA was sold to Syncapay, Wirecard AU was sold to Change Financial etc.

Since Delaware does not reveal the shareholders of a local corporation, how exactly have you figured out who owns Qenta Inc?

Within your screenshot of Qenta GmbH, it just shows that Kerim Chouaibi is the director of that German entity. So how does this provide evidence of him being the shareholder of either company?

Because the liquidation process could have been done more effectively, and, from provided information on 9Fraud, there was not really enough reason to block Qenta's acquisition and continuation of EPB business especially since there was going to be an immense capital increase that would protect clients.

Attachments

What is so difficult to understand? Have you never heard of a rebrand?Here we have this article about Emergent Technologies and Qenta. Mentioning Brent de Jong as CEO of EmTech and Kerim Chouabi, CEO of Qenta CEE.

https://www.prnewswire.com/news-rel...logy-driven-payments-solutions-301482341.html

EMERGENT TECHNOLOGY & PAYMENTS INC. = QENTA INC. (Company No. 6227324)

Kerim Chouaibi is the director and CEO of Qenta CEE which is a tech company they acquired from Wirecard during its liquidation. So what? This means nothing.

Yes, Emergent Technology Holdings LP is used, as can be inferred from its name, as a holding company for Qenta.This article is from February 2022, so before the welcome letter we received. (The news about EmTech end in February 2022: https://www.prnewswire.com/news/emergent-technology-holdings-lp/)

LPs are normal for equity funds, holding entities, etc. in the US. So what?

Yes, it's registered in Delaware and has offices in Houston.This welcome letter stated that Qenta is a company based on Houston TX.

BdJ personal HoldCos are also in TX.

Proof?That is not correct! Instead Brent de Jongs company resides there: https://contactout.com/Brent-De-Jong-7692123. So the clients of EPB were sent a welcome letter of Qenta (even with their brand name on top), but the company they were actually referrring to was the company of BdJ.

What false premises?So one can say, that this information at least was wrong! Which raises the question whether the agreement of the former EPB-clients to opt-in was based on false premises?

Why would it have failed?And it also raises the question, whether the oversight of the OCIF in this process has failed?

Using Delaware for a corporation is completely normal.

Qenta also has its subsidiary in PR.

There are things to attack Qenta for: their UAE trade licenses have expired, their Swiss company is closed, they only have an MSB and licenses in low-tier countries in places like Ghana or Bosnia and Herzegovina.

But the apparent non-existence of their entity, the doubt for which was only created because people, for some unknown reason, cannot comprehend that an entity can change its name, is really not one of them.

You already shared this before – it shows Kerim is the director of the Austrian entity. This is NOT a financial company and cannot hold customer funds (there are no statements or evidence for it doing that either).

This does not show ownership at all.

Schiff´s comment "Qenta was setting up accounts for each Opt in customer" is meaningless,nowhere in the September 2022 agreements is fund segregation mentioned. This omission was convenient. Let’s be real: Qenta wouldn’t have paid $1.25M if Schiff/EPB had properly demanded segregation in writing.The losses related to losses that Qenta may incur as a result of acquiring the assets. It has nothing to do with bank customer's losses. Again, Qenta was setting up accounts for each Opt in customer. Qenta was going to convert all deposits into gold, via G-coin. That would have worked out well. Gold was $1,800 an ounce then. Now its $2,900. Customers would have left the gold in their G-coin wallets, or liquidated it and withdraw the balance in cash to any alternative financial institution. That was the plan. The Portugese Government got in the way due to the fraud committed by the OCIF Commissioner, the IRS, the other J5 Chief, and the media.

However, it looks like if anyone sues me or the bank for losses that related to the opt in customers, than Qenta has indemnified us for those losses. But the only way Opt in customers will lose money is if Qenta goes bankrupt before you get it back. In which case their indemnification will be worthless. However, according to the Qenta CEO, the company is not in financial trouble and is prepared to return all funds to customers.

Another likely lie: Section 2.1 of the September 30, 2022 agreement states that $1.25M was due as:

- $500K paid immediately after G-Commerce’s Letter of Intent.

- $750K payable within 15 business days after closing.

Again, the payment went to the bank, not me. I never got a dime. Plus only $500K was paid.Absolutely correct! And EPB even had the audacity to provide its clients with wrong informations about Qenta (see my post above), while OCIF obviously did not pay attention to this fact!

Share:

Latest Threads

-

Selling weight loss medicines online

- Started by daggerbackstage

- Replies: 0

-

Hungary criminalizes unapproved crypto trades

- Started by toums

- Replies: 1

-

Hiding US LLC profits by electing for corporation tax treatment

- Started by Eurocash

- Replies: 8

-

-

Company formation for a specific niche without licenses

Company formation for a specific niche without licenses- Started by luxtravel

- Replies: 10