Correct, the bank was closed solely as a publicity stunt for the J5. It was arranged by the IRS and secretly agreed to by the OCIF Commissioner. She had originally told all the parties she was going to approve the sale to Qetna. For seven months we all proceeded under the impression the sale would go through. However, sometime in March of 2022 the IRS got the OCIF Commissioner to change her mind, reject the sale she had planned to approve, and hold a press conference three months later to allow the J5 to take credit for the closure and pretend the bank was guilty of the very crimes its own investigation proved it did not commit. This was also done to help the Australian reporters defend against my defamation lawsuit. They introduced the closure of the bank as evidence, but the judge didn't buy any of it. Nine lost my defamation lawsuit anyway. They had no evidence the bank actually did anything wrong.If every bank that had regulatory issues were to be closed we would not have any banks today. The fact that a bank like Silicon Valley was forcefully bought while EPB was not allowed to be sold suggests that regulation was not a major factor in these cases. OCIF could have came up with other nonsense to close the bank, like not vetting clients which is an arbitrary demand subject to the agencies desired end goal. They just went with the easiest solution to close the bank the J5 wanted to kill, of which they proudly and publicly supported.

Our valued sponsor

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Euro Pacific bank is a scam

- Thread starter sonato

- Start date

-

- Tags

- euro pacific bank

Does this mean that the opt-ins are fully covered but the opt-outs might not be?The money at Novo Bank never went to Qenta. The Receiver finally transferred it to a bank in California. Qenta got the money that was on deposit at IB, which was more than enough to cover all opt ins. So now it needs to transfer the excess back to the bank to cover the opt outs.

From what I understand all customers will be treated equally. That is part of what is supposedly holding up the return of customer funds. They need to make sure everyone recovers the same percentage of their deposits, in case there is no enough left to cover 100%.Does this mean that the opt-ins are fully covered but the opt-outs might not be?

Yes, this logic definitely makes sense. However, if we gear in, the next (sensible) question is: why not return what is already available, e.g. 90 % on a per capita basis and wait for the rest ? It would only cost one wire each one. So what ?From what I understand all customers will be treated equally. That is part of what is supposedly holding up the return of customer funds. They need to make sure everyone recovers the same percentage of their deposits, in case there is no enough left to cover 100%.

Anybody's guess ?

")

Creditors aren't payed the same amount or percentage normally so I guess there is no such rule. There's a hierarchy of who gets payed first and who last or not at all.

yes, but we customers, both opt-ins and outs, should be all on the same level I guess.Creditors aren't payed the same amount or percentage normally so I guess there is no such rule. There's a hierarchy of who gets payed first and who last or not at all.

You are. You also come before other creditors. When the bank went into foreclosure there were about $500K in trade payables. I reduced that $300K for quick payments. But the receiver refused to authorize payments. So my guess is none of these creditors will be paid unless customers are made whole. At the time I negotiated those discounts, there would have been $ 2-$3 million in cash left over after all depositors where made whole. But given the delay I have no idea if any money will be left over for me, or if depositors will be made whole or not. If they are not other creditors will get nothing, and neither will I. However the bills the receiver incurs after he took over get paid, as does the receiver himself. They take priority.yes, but we customers, both opt-ins and outs, should be all on the same level I guess.

No comment.....However the bills the receiver incurs after he took over get paid, as does the receiver himself. They take priority.

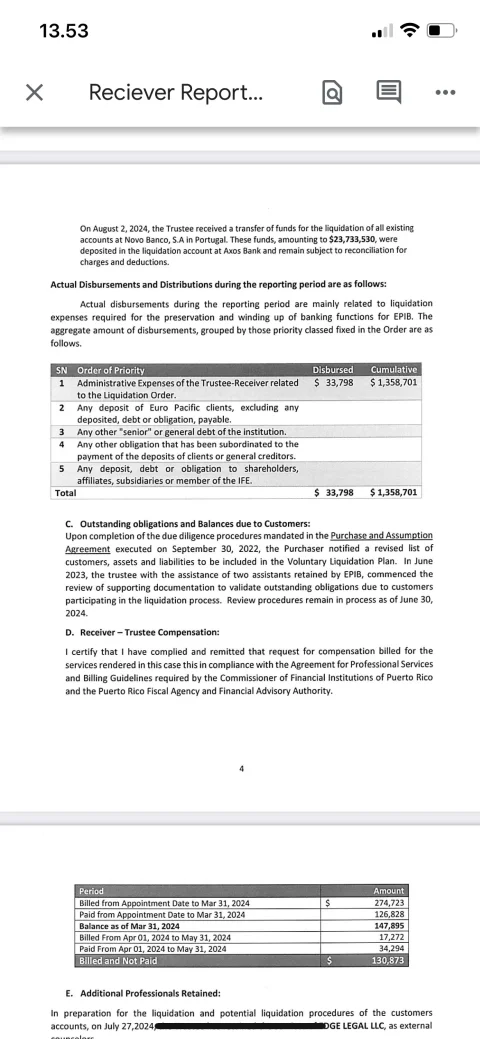

As I understand the latest reciever report, he has spent USD 1,358,701 in total including his own fees. So if there were 2-3 million in excess cash in EPB I think it’s beginning to dry up and after that he will surely tap into customer deposits ..You are. You also come before other creditors. When the bank went into foreclosure there were about $500K in trade payables. I reduced that $300K for quick payments. But the receiver refused to authorize payments. So my guess is none of these creditors will be paid unless customers are made whole. At the time I negotiated those discounts, there would have been $ 2-$3 million in cash left over after all depositors where made whole. But given the delay I have no idea if any money will be left over for me, or if depositors will be made whole or not. If they are not other creditors will get nothing, and neither will I. However the bills the receiver incurs after he took over get paid, as does the receiver himself. They take priority.

Attachments

Correct. That figure includes the $1.25 million that was to be paid to the bank by Qenta. The first $500K was received. The rest is still due. The receiver did blow a $500K receivable though gross negligence. So we lost that money. Also there was a $300K bogus fine that was owed to OCIF. It was for operating the bank without a license. Though the bank filed its 2022 renewal on time, and paid the annual fee, OCIF decided to reject the renewal over 5 moths after it was filed, and retroactively fine the bank $5K per day for unknowingly operating without a license. The original fine was $700K, but I negotiated it down. I think the sole reason for the fine was to make the bank look bad in the media, as the fine was a big part of the stories that where written. Of course it also generated revenue for OCIF.As I understand the latest reciever report, he has spent USD 1,358,701 in total including his own fees. So if there were 2-3 million in excess cash in EPB I think it’s beginning to dry up and after that he will surely tap into customer deposits ..

Thank you for posting that.

Hopefully this is the last chapter.

Let's see how much money we get back....

Yes, thank you for sharing!"While we cannot provide a firm timeline at the moment, all efforts are geared to commence this

liquidation process within the next upcoming weeks"

However, I remember having seen this phrase over a year ago. So, for the time being, that makes me a beautiful leg

") . Explanation: this is what we call FrEnglish and

. Explanation: this is what we call FrEnglish andconsists in "translating" a French expression by just substituting words. "Ca me fait une belle jambe" in fact means something like "So what? That does not affect me at all"

Hopefully "commence the liquidation process" isn't just the beginning of a long, drawn out process. Frankly I thought the liquidation process began over two years ago. Apparently it's only just beginning now. I hope customer funds are returned within the first few months of this process. Hopefully what was intended to be a 90 day process, with 100% of customer funds returned in the first 30 days, will be wrapped up in under three years.

Very much so, Peter !Frankly I thought the liquidation process began over two years ago

"Hopefully, what was intended to be a 90-day process, with 100% of customer funds returned in the first 30 days, will be wrapped up in under three years."

Plus a year or so of investigation, to catch the dangerous TE, TF and ML, yet to be seen. That changed considerably the Bank's

quality of service - I could feel it. What a shame indeed !!

The bank went into Receivership to be liquidated. The receivership process had begun two years ago which leads to liquidation process. This is normal order of events btw.

Receivership

Legal process where a receiver is appointed to take control of a company's assets and manage its affairs.Liquidation

Process of winding up a company's affairs and distributing its assets to creditors and shareholders.This might be true under a normal situation where a bank goes into receivership because its actually bankrupt. Therefore there is a lot to sort out and unwind. But in this case the bank was only put into receivership as a PR stunt. It was completely solvent. There were no loans to sell off, no debts to repay. The cash alone balance sheet exceeded all monies owed. The only liability on the balance sheet other then a few hundred K in outstanding bills was the money owed to depositors. It was likely the simplest bank liquidation in history. It should have been able to have been done in one day.The bank went into Receivership to be liquidated. The receivership process had begun two years ago which leads to liquidation process. This is normal order of events btw.

Receivership

Legal process where a receiver is appointed to take control of a company's assets and manage its affairs.

Liquidation

Process of winding up a company's affairs and distributing its assets to creditors and shareholders.

Where does it read that? Can you post the document?According to IRS documents the bank was liquidated months ago.

Share:

Latest Threads

-

How to Open a Bank Account in Mexico for Residents & Non-Residents

How to Open a Bank Account in Mexico for Residents & Non-Residents- Started by Kim-OTC

- Replies: 0

-

How Do You Open a Bank Account? Requirements, Considerations & Precautions

- Started by Kim-OTC

- Replies: 0

-

-

Compte Offshore En Ligne & Other Forms of Offshore Bank Accounts Explained

- Started by Kim-OTC

- Replies: 0

-

Can anyone help me with processing credit cards to get Crypto?

- Started by Moskva777

- Replies: 0