Does Cyprus really controls if you spend more than 183 days in another country ?

Many accountants told me I have to keep tracks of my movements all over the year which i think it's crazy

Does Cyprus really controls if you spend more than 183 days in another country ?

if I work with the offshore and I exceed 35k, do I have to declare and then pay 5k?

or working offshore is it better not to say anything to the Maltese state?

Aren't those estonian's CFC rules? Since you are maltese non-dom shouldn't you care about maltese CFC rules?The Estonia company will be considered a CFC in Malta and treated as such but you have the following exception or threshold:

The CFC rule shall not find application in relation to an entity or permanent establishment:

- with accounting profits of no more than EUR 750,000 and non-trading income of no more than EUR 75,000;

Aren't those estonian's CFC rules? Since you are maltese non-dom shouldn't you care about maltese CFC rules?

Interesting. They replied that they don't enforce POEM, or you had special circumstances?But according to their tax government it shouldn't be an issue (they replied like this via email)

Martin, i verified before posting.These are Maltese CFC rules.

Can you be more specific?But according to their tax government it shouldn't be an issue (they replied like this via email)

I asked directly to the Maltese government about this issue, this is what they answeredMartin, i verified before posting.

Take a look: those are Estonia CFC rules and those are Maltese CFC rules.

The 750K limit / 75K passive income limit are for Estonian CFC.

Can you be more specific?

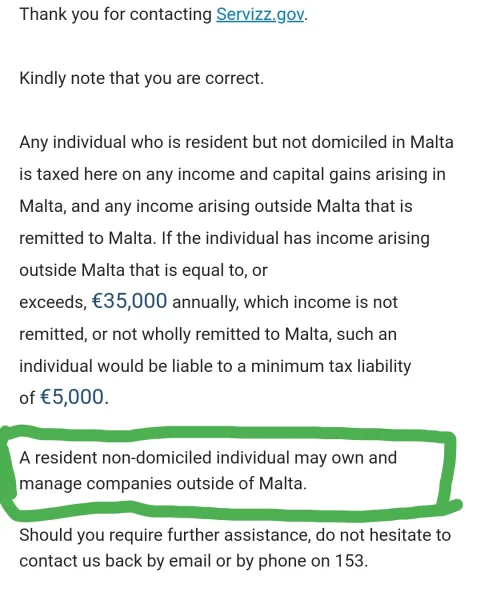

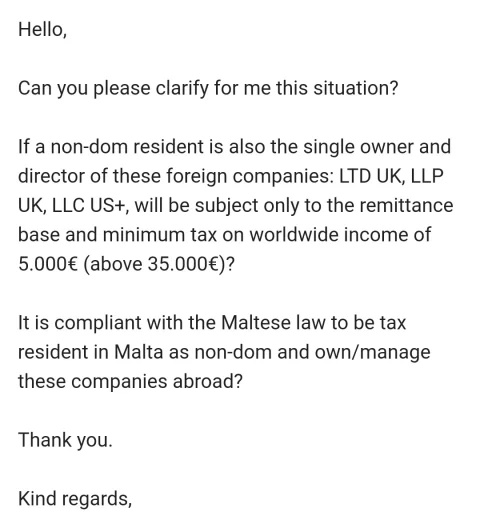

This was my question, however regarding pass-thru companies like the LLP UK or LLC us i still have doubts it can work, because yes you can own and manage them as they said, but you will be then theoretically subject to the local normal tax rate, as this income is considered personal. So what i understand here is that there are no issues to own a manage a company located abroad but better to choose an ltd (UK, Bulgaria, Romania, Estonian, etc) and it should work just fine.I asked directly to the Maltese government about this issue, this is what they answered

Amazing!I asked directly to the Maltese government about this issue, this is what they answered

That's true but in their answer they talked about "income arising outside Malta" so maybe it could be worth double checking with them asking specifically if a non-dom could manage a transparent entity like UK LLP and his taxation be limited to 5K annually if foreing income > 35K.this income is considered personal.

They write manage it outside Malta.I asked directly to the Maltese government about this issue, this is what they answered

A company incorporated outside of Malta is considered to be resident in Malta only if its place of effective management and control is in Malta. As a general rule, ‘the place of effective management’ is defined as the place where the key management and commercial decisions that are necessary for the conduct of the company’s business are in substance made.They write manage it outside Malta.

Martin, i verified before posting.

Take a look: those are Estonia CFC rules and those are Maltese CFC rules.

The 750K limit / 75K passive income limit are for Estonian CFC.

.

.Can someone explain what does it means a non trading income of no more than 75,000€? Trading stocks or is something else?I have no idea why you keep questioning me.

https://www2.deloitte.com/mt/en/pag...AD-implemented-into-Maltese-domestic-law.html

----

CFC rule

In terms of the ATAD Implementation Regulations, the CFC rule shall find application where the following conditions are met:

Should an entity or permanent establishment be treated as a CFC, the non-distributed income of the said entity or permanent establishment arising from non-genuine arrangements which have been put in place for the essential purpose of obtaining a tax advantage shall be included in the tax base of the taxpayer. The income to be included in the tax base of the taxpayer shall be limited to amounts generated through assets and risks which are linked to significant people functions carried out by the controlling company.

- control test (in case of an entity): the taxpayer by itself, or together with its associated enterprises holds a direct or indirect participation of more than 50% of the voting rights, or owns directly or indirectly more than 50% of capital or is entitled to receive more than 50% of the profits of that entity; and

- low-taxation test: the actual corporate tax paid by the entity/permanent establishment is less than 50% of the tax that would have been ‘charged’ on the entity or permanent establishment in terms of the ITA.

The CFC rule shall not find application in relation to an entity or permanent establishment:

-----

- with accounting profits of no more than EUR 750,000 and non-trading income of no more than EUR 75,000; or

- of which the accounting profits amount to no more that 10% of its operating costs in the tax period.

Even the PWC link you posted stated this but didn't give the figures:

"CFCs whose profits fall within certain minimum thresholds are excluded from the application of this regulation"

In fact just google "malta CFC 750,000". Maybe they all have it wrong then

Even stated below etc:

https://www.dmeurope.eu/blog/controlled-foreign-company-cfc-malta-eu-atad/

----

Exceptions to the rule

A CFC that satisfies the following criteria would not be charged to tax in Malta:

-----

- CFC with accounting profits of no more than €750,000, AND non-trading income of no more than €75,000; OR

- CFC of which the accounting profits amount to no more than ten per cent (10%) of its operating costs for the tax period, Provided that the operating costs may not include the cost of goods sold outside the country where the CFC is resident for tax purposes AND payments to associated enterprises.

. So back to topic.If you are resident non-dom in Malta, manage an offshore compay and that company's accounting profits are less than 750k and passive income (royalties, trading) are less than 75K you only pay the 5K minimum tax per year in Malta. The downside is that you have to be there at least 183 days per year which for somebody could be a deal breaker.So can you please explain me what did you understand, iin simple words?

Strangely enough they don't talk about the 750k in the country highlights for 2021. Back to topic.Deloitte does talk about 750k I even posted it and quoted them above.

Yes but the 183 days rule it's not strictly enforced there, like in many others countries like Romania and Bulgaria for exampleIf you are resident non-dom in Malta, manage an offshore compay and that company's accounting profits are less than 750k and passive income (royalties, trading) are less than 75K you only pay the 5K minimum tax per year in Malta. The downside is that you have to be there at least 183 days per year which for somebody could be a deal breaker.

Strangely enough they don't talk about the 750k in the country highlights for 2021. Back to topic.

. The motive for such a move would be the EU's (via OECD) continued attacks to destroy all tax havens.

. The motive for such a move would be the EU's (via OECD) continued attacks to destroy all tax havens.