Thank you, although that option does not seem to be tax-free from what I've just read.

No, because this is your interpretation of that screenshot and you have not corroborated with any other evidence so far and I cannot corroborate it either and I'm doing quite extensive research since you first mentioned this because this is true, then it will obviously impact the answer to my original question. It does not seem you are speaking from experience specifically with Mobile Apps.

Needless to say, it's an absolutely crucial point whether any kind of 30% Withholding Tax is charged on App Sales, Ads, and/or in-App purchases. That's why I'm making a point of being precise so that we do not spread misinformation.

It honestly does not seem like you yourself are certain that App are subject to such tax in some circumstances as it seems you are making an assumption based on what you've seen elsewhere in relation to Youtube. But assumptions will not help those researching the most tax-friendly jurisdiction for their App business because it can lead to incorporating in the wrong place and paying taxes that are not necessary.

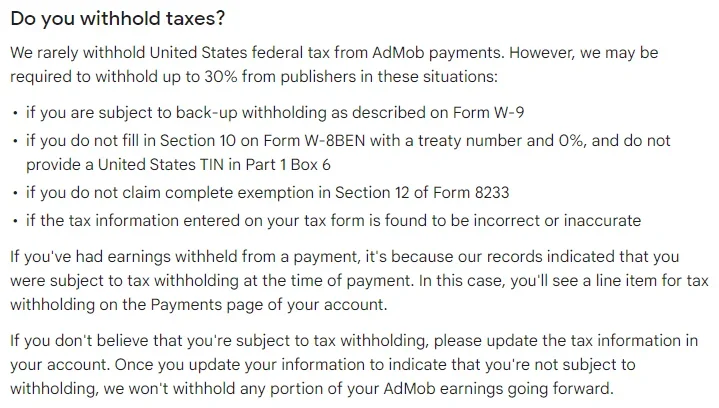

For example, Apps tend to use Admob (not Adsense) for Ads, and this is what Google's site says about that:

View attachment 4084

View attachment 4085

View attachment 4086

https://support.google.com/admob/answer/4381375?hl=enhttps://support.google.com/admob/answer/2772627

So the above hard evidence contradicts what you are saying about Mobile Ads in Apps being subject to 30% Withholding Tax for people with no US Activities like myself.

Surely if the Apple and Google Play Stores were Withholding 30% of any kind of revenue from Apps for US Tax purposes from companies based outside of the US, this would be all over the internet and therefore very easy to corroborate directly instead of via a screenshot from Youtube's tax info. So for the sake of all readers, I am extremely skeptical of the claim that Apps by people with no US Activities are subject to any kind of 30% Withholding until I see hard evidence, which no one has provided yet and which I myself have been unable to find so far.

I don't feel entitled to anything. I'm providing a lot of my own research and evidence as well. But if someone states something without backing it up which contradicts what I am finding, then of course I'm going to ask for proof. So please don't confuse my push for precision to avoid misinformation with entitlement. No one is forced to answer just like I am not forced to accept assumptions or anonymous statements online as fact. Misinformation on something as crucial as this can damage a lot of people.

Please provide

evidence of this. All the evidence I am finding for the withholding of 30% from US users for foreign businesses is related to Youtube's recent changes (stated clearly

here), not Apps.

This contradicts what

@marzio mentioned above that the Sales themselves are not subject to Withholding Tax because they are not treated as Royalties. Again, this is why being precise with something so crucial is so important, and why such statements need to be corroborated with hard evidence.

This assumes you are correct that "

US app sales from the playstore will be withholding 30% (Only US Sales)!", but that does not seem to be correct. First we need to confirm that App Sales, Ads, and/or in-App purchases are indeed subject to any kind of 30% Withholding Tax before we can cross this bridge.

Again, something as significant as that should be easy to corroborate, but I am not finding any hard evidence that the App Stores charge any kind of 30% Withholding Tax to non-US companies their App Sales, Ads, and/or in-App purchases revenue.